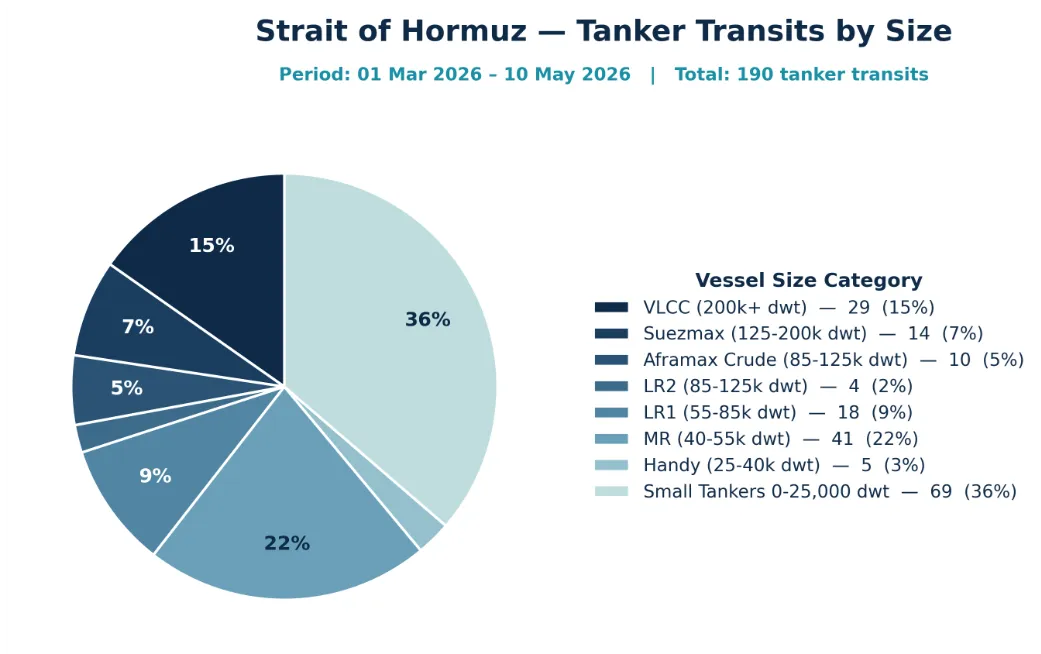

Asia is facing a sharper inventory squeeze as Hormuz disruption keeps oil import flows under pressure, pushing greater reliance on strategic and commercial stocks to support domestic supply. The report notes tanker crossings through the Strait remained very limited across the period reviewed, with the trend weakening sharply from late April into early May and the steepest drop in the most recent week.

Reserve coverage across Asia is uneven, with deeper buffers in Japan and South Korea and very large strategic and commercial inventories in China, while several South and Southeast Asian economies remain more exposed with thinner reserve protection.

The result is rising supply strain and higher import costs across parts of South and Southeast Asia, against a backdrop of higher oil prices, firmer freight and ongoing inventory draws.

Capesize average earnings were $41,400/day with the BCI at 4,960, up 11% w-o-w. Panamax average earnings were $20,100/day with the BPI at 2,230, up 12% w-o-w. Supramax average earnings were $19,200/day with the BSI at 1,520, up 0.1% w-o-w. Handysize average earnings were $15,000/day with the BHSI at 833, up 2% w-o-w.

Capesize strengthened on Brazil and West Africa to China, with C3 at $35.5/ton and a 182,000 dwt fixed Tubarao with West Africa option to Qingdao at $36.75/ton.

Panamax firmed on improving NCSA grain activity and tighter tonnage, with an 82,000 dwt fixed delivery Gibraltar for a fronthaul trip at $25,000/day.

Supramax stayed mixed as the US Gulf lost momentum while the South Atlantic held support, with a 56,000 dwt fixed Med to East Coast India with fertiliser at $18,000/day.

Handysize remained supported from the US Gulf and South America, with a 40,000 dwt open Lagos fixed for a trip delivery Vila do Conde to Norway with alumina at $22,000/day.

Capesize remained supported by steady miner activity and healthy cargo flow, with C5 at $15.2/ton and a 180,000 dwt fixed Port Hedland to Qingdao at $15.5/ton.

Panamax stayed firm on steady coal and mineral demand and tighter prompt tonnage, with an 82,000 dwt fixed open Songxia for an Australian round voyage at $23,000/day.

Supramax saw softer enquiry in the north with better demand further south, including a 64,000 dwt fixed delivery North China for redelivery Sri Lanka at $23,000/day.

Handysize held a steadier Far East tone on tighter prompt availability, with a 37,000 dwt fixed for multiple trips from CJK at $17,500/day.

VLCC firmed, with TD15 (West Africa to China) at $121,500/day and TD22 (US Gulf to China) at $112,400/day.

Suezmax firmed, with TD20 (West Africa to UK Continent) at $85,000/day and TD27 (Guyana to UK Continent) at $85,650/day.

Aframax softened sharply, with TD25 (US Gulf to Continent) at $69,700/day and TD26 (EC Mexico to US Gulf) at $102,300/day.

LR2 softened, with TC20 (MEG to UK Continent) at $147,200/day.

MR remained under pressure, with TC21 (US Gulf to Caribs) at $17,300/day and TC2 (Continent to US Atlantic Coast) at $17,400/day.

VLCC firmed in the Gulf, with TD3C (MEG to China) at $458,200/day and TD34 (Gulf of Oman to China) assessed at WS147, equivalent to $26.75/ton.

Suezmax saw limited visible AG/Red Sea fixing during the week.

Aframax remained pressured in the Med, with TD19 (Cross-Med) at $72,600/day.

LR rates softened, with TC1 (MEG to Japan) at $149,600/day and TC5 (MEG to Japan) at $117,000/day.

MR softened, with TC7 (Singapore to ECA) at $38,100/day.

Over the past twelve months, Greece led reported secondhand selling with 319 vessels, versus 165 for China. Greek sales were led by 150 dry bulk and 122 tankers, plus 32 containers and 10 gas carriers, while Chinese sales comprised 107 dry bulk, 36 tankers, 12 containers and 5 gas carriers.

On the buying side, Greece recorded 234 purchases and China 213, with Greek buying led by 121 dry bulk and 85 tankers and Chinese buying led by 165 dry bulk and 35 tankers.

This post provides a high-level overview of the emerging global inventory squeeze, Asian reserve exposure, and current freight market performance.

The full Allied QuantumSea Weekly Market Report – Week 19 includes:

In-depth analysis of strategic petroleum reserves and commercial stock pressure

Assessment of Asian oil inventory coverage and import vulnerability

Hormuz disruption impacts on crude flows, freight costs and supply security

Dry bulk and tanker earnings tables across all vessel classes

Atlantic & Pacific route-level freight analysis with fixture benchmarks

Baltic indices, TCE calculations & historical trend comparisons

Secondhand S&P transactions, buyer–seller positioning & asset value trends

Recycling activity and scrap pricing indicators

👉 Fill in the form below to subscribe and receive the complete PDF directly in your inbox every week.