Shipping is a capital-intensive industry where access to competitive ship finance influences the pace of fleet renewal, growth and modernization. Ship financing — most commonly through loan and leasing instruments — is deployed to acquire vessels, refinance existing loans, or to optimize a company’s capital structure.

From single-asset deals to fleet financing schemes, shipowners balance leverage, tenor, repayment profile, pricing, and covenant flexibility against earnings capacity and potential capital gains over the desired investment horizon.

Debt instruments are sourced globally from international banks, regional lenders & other financing institutions, non-bank lenders, credit funds and leasing providers, all of each provide debt instruments typically in the form of mortgage-backed loans or leasing instruments.

In practice, the optimal capital structure blends leverage, corporate recourse or absence thereof, structural flexibility and repayments that may be supported by fixed contractual cashflows stemming out of period charters, all of which weight against the availability of different financing options for a given shipowner profile and reflect on their cost.

Allied QuantumSea supports its shipowner clients through a complex, multi-dimensional financing landscape end-to-end—structuring, negotiating, and coordination the execution of debt or leasing facilities that align with the envisaged investment strategy and optimal capital structure sought.

Shipowners and investors can access a host of financing tools:

Amortizing term loans are widely used ship financing instruments providing leverage in the region of 50- 65% of the fair market value of a ship and secured in favor of the lender with first priority mortgage on the ship, assignment of earnings & insurances, pledge of the shares in the shipowning SPV.

The structure may also embody a guarantee either from the management company of the ship or from a holding company consolidating all or substantial parts of the assets of a shipowning group, in which case the security structure may also embody certain financial covenants. Term loans provide a lower-leverage lower-interest cost proposition compared with other financing options.

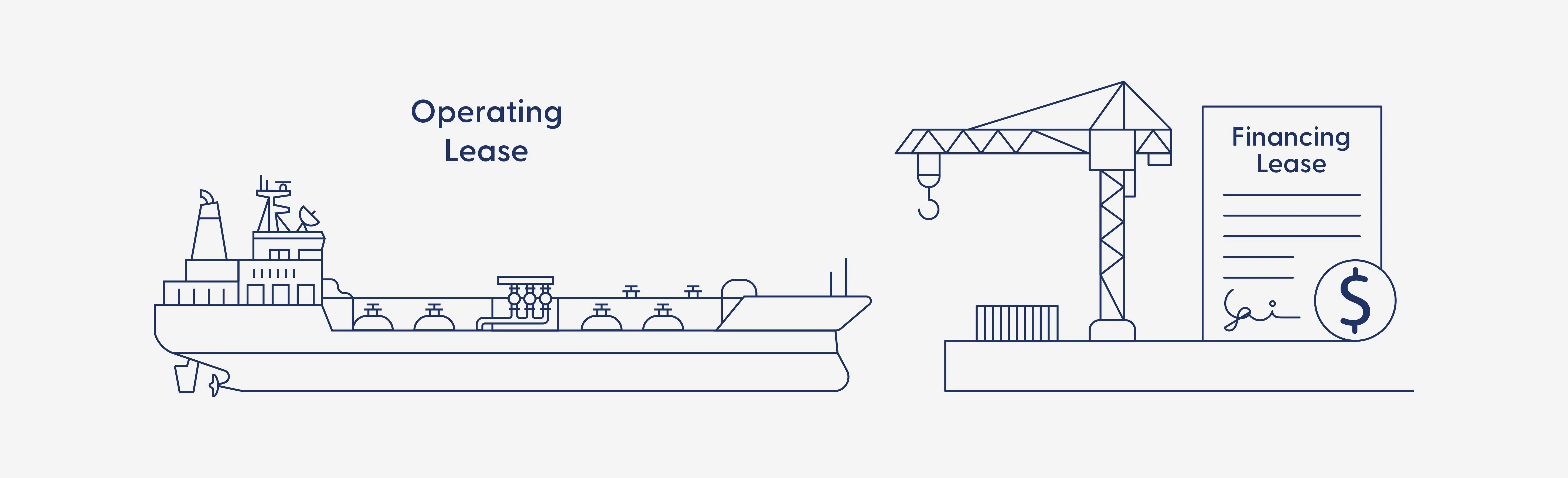

Leasing solutions transfer legal title of the ship to a lessor while control over operational, technical and commercial matters resting with the shipowner / operator. Leasing is another common form of widely-used debt instrument in shipping - typically in the region of 70 - 85% of the fair market value of ships - leverage, yet higher-cost proposition or in the case of smaller, weaker or start-up shipowning endeavors offering access to ship financing which would otherwise be unattainable.

Within leasing, Japanese Operating Leases with Call Options (JOLCOs) combine tax-efficient equity sourced from Japanese investors which - combined with bank debt – is packaged and offered to takers of these leases – shipowners – in structured known for their financial flexibility underlying by the lack of restraining financial covenants or security value maintenance clauses which could otherwise cause significant obligations for additional collateral in the case of drop in the market values of the financed ships.

Bareboat Hire Purchase agreements (BBHPs) combine the flexibility of leasing with other advantages relating to deferred payment of a significant portion of the purchase price of ships several years down the line at pre-specified levels with the balance being paid upfront and another portion being amortized in the course of the tenor of the bareboat charter and paid as bareboat charter hire.

Financing strategies differ for newbuilds versus second-hand ships, for different ship types, shipowner profiles, aggressive or conservative investment strategies, risk-reward appetite and other factors including trading, commercial and environmental characteristics.

Newbuilds may pair commercial tranches with export credit support; second-hand acquisitions often prioritize speed to close and delivery-aligned drawdown. Another key distinction is recourse vs. non-recourse. Bank loans frequently require recourse to holding company guarantees or cross-collateralization, lowering cost but increasing sponsor exposure. Non-recourse or limited-recourse leasing is offered at higher pricing in exchange for ring-fencing risk at the asset or SPV level.

Allied designs structures that take into account the desired balance-sheet strategy, shipowning profile and track record of the operator with a view to optimizing proceeds, pricing, and financial flexibility.

Capital allocation is as important as capital access. Lower-leverage, lower-cost bank debt can maximize long-run returns through reduced financing expense and lighter cash-flow stress—particularly valuable in volatile freight markets. Conversely, higher-leverage, higher-cost leasing structures can accelerate growth, amplify equity IRRs in strong cycles, and preserve corporate liquidity—at the price of tighter residual obligations and debt servicing strain in downcycles.

Allied’s capital allocation advisory quantifies these trade-offs across different leverage and pricing scenarios, comparing recourse structures including holding company guarantees if available with ring-fenced non-recourse options.

By embodying relevant sensitivity scenarios, we set forward responsible recommendations on optimal investment strategies supported by viable capital structures tailored around specific risk-reward investor profiles.

Shipping financiers operate within regulatory frameworks that shape pricing, leverage, and eligibility. EU, US, and Chinese regulations drive bank capital requirements, client and country risk concentration limits, and define portfolio risk weightings — affecting appetite for older tonnage, spot-exposed assets, and higher-emission profiles.

ESG is increasingly embedded: green shipping finance and sustainability-linked features reference measurable KPIs (e.g., CII trajectories, EEOI improvements, verified emissions reductions), with margin step-downs for outperformance and step-ups for underperformance.

Across all facilities, compliance with Anti-Money Laundering (AML), Know Your Client (KYC), and background checks ensure counterparties, physical UBOs, and sources of funds adhere to EU, US and UN sanctions. Engagements are verified at mandate and monitored post-closing, while we abide to documentation and processes reflecting these realities, minimizing execution friction, reputational exposure and maximizing lender readiness as from the outset.

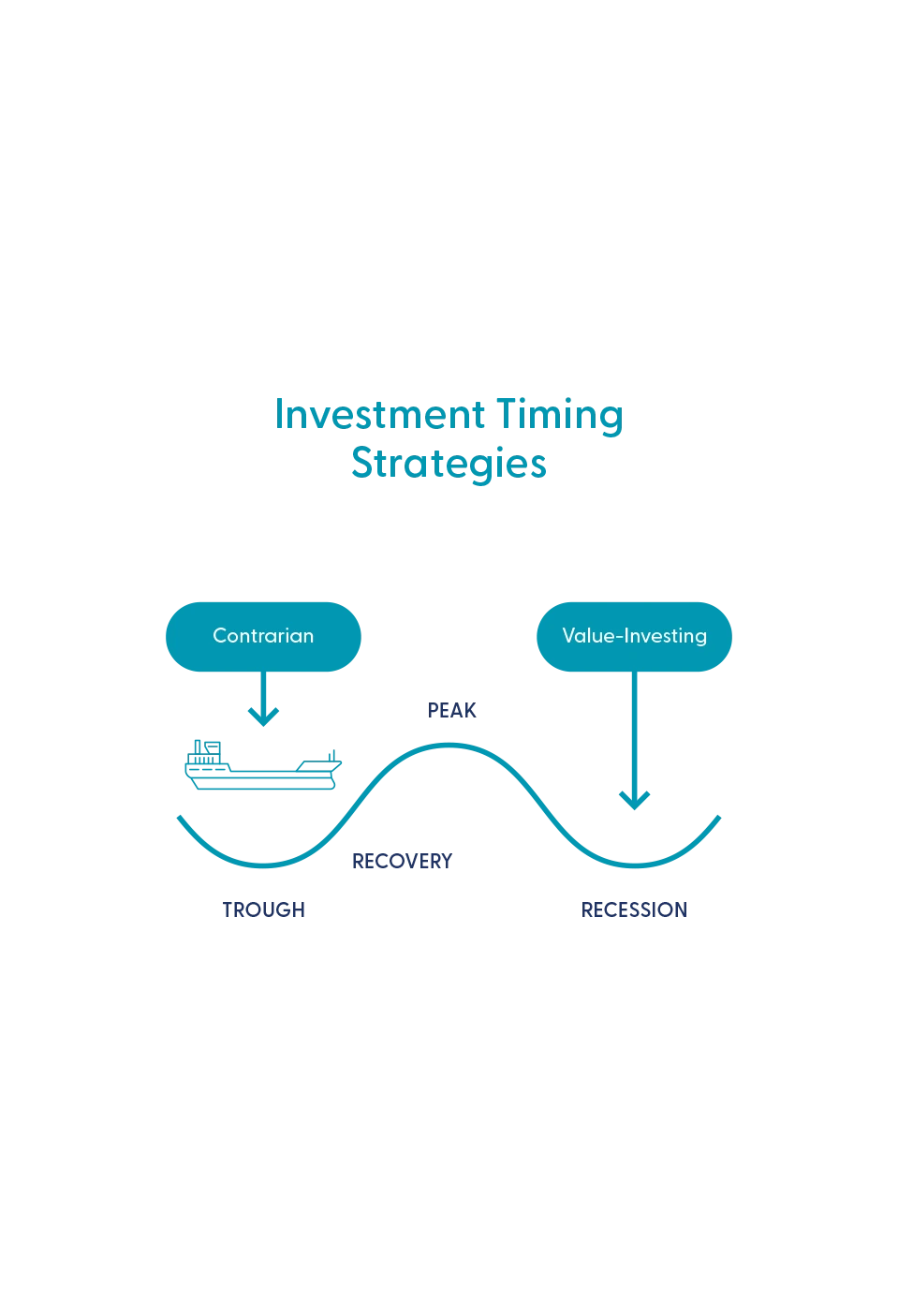

Shipping market outlook, global trade shifts, fleet age profile, newbuildings orderbook and delivery schedule and ship recycling, all key factors affecting the shipping market supply – demand balance, interact with credit cycles in shaping ship lending cyclicality.

When freight is firm and asset values high, liquidity typically expands; during softer periods, lenders focus on charter cover as part of cashflow stability and visibility, sponsor strength, and lower LTVs as ways to manage their credit exposure. The recent buoyant market across the majority of dry bulk, tankers and container market sectors post covid has led to significant cash accumulation on the part of owners, leading to reduction in demand for new financing, early repayments in part or as a whole of existing facilities, and refinancing at better terms.

Interest rates in shipping directly influence debt servicing ability and prompt borrowers to fic interest in low-interest rate environments. Environmental policy and regulations filters into underwriting via higher capex for newbuilds for eco features or retrofits to existing ships that substantiates higher market values, while differentiated credit policies exist across different types of lenders in support of modern or legacy tonnage.

For owners, this means that timing matters: refinancing at the present competitive financing environment can open the door to new lending relationships, lead to better terms including reduced interest costs, and may release equity for deployment in new, counter-cyclical acquisitions with conservative leverage as means to compound value.

Allied develops pointed financing recommendations taking into account the profile of the shipowner, the specific forward- looking investment aspirations of the underlying sponsors and the optimal longer-term capital allocation strategy.

Before approaching financing institutions, shipowners should define corporate architecture and risk appetite. Individual shipowning SPV setup presents a simple structure where liabilities are ring-fenced down to each single asset.

Holding company corporate setups consolidating group assets and guaranteeing the performance of individual ship-owning borrowing companies to lenders unlock access to a wider spectrum of financing options at most competitive terms and lowest possible pricing.

In terms of the desired financing strategy, this may be opportunistic with high-leverage, often suited to short-cycle plays, smaller, weaker borrowing schemes or newcomer shipowners with limited financial means. In contrast, long-term, relationship-driven financing strategies typically focus on repetitive borrowing in the longer run from a group of financing institutions where mutual trust is being built over time for the benefit of retaining uninterrupted access to financing while optimizing cost and accommodating specific sensitivities of the underlying borrowing group.

Lenders give regard to fixed, contractual cashflows (mid- to long-term charters, COAs) from reliable, trustworthy counterparties with proven track record as means for enjoying revenue stability & visibility, in return for which they offer higher loan advances at lower interest costs while opting to de-risk the structure with steeper repayments tailored around the terms of the underlying employment.

Allied advises shipowners for the optimal financing strategy in meeting defined investment goals and assists in identifying and implementing the required milestones.

Shipping finance involves several parties with aligned incentives in executing promptly on financing schemes.

Shipowners as borrowers articulate strategy, set out the key financing requirements, invest equity in the projects and in most cases provide operational, technical and commercial management of the financed ships.

Financing institutions which include international banks, regional lenders, non-bank lending platforms, credit funds, export credit agencies and lessors supply capital in the majority of the cases on the basis of asset-backed, senior-secured debt instruments typically reflecting loans or leasing structures.

Specialized maritime legal counsels draft loan, lease, security, corporate and vessel documentation.

Technical consultants conduct vessel inspections and condition surveys as part of the facility drawdown process or for the purposes of collateral monitoring of the financing providers.

Allied acts as financing advisor, arranger and process coordinator assisting in the identification of the optimal source of capital, helping with negotiations, and running a competitive financing process with a view to sourcing best terms. Operational Lease Financing Lease

Allied builds integrated ship financing models with cash flow modeling, debt break-even calculations, financial covenant stress testing with sensitivities on a number of key factors including residual value at the end of the envisaged investment period, freight revenues, OPEX, and any other material aspects that may impact investment performance. We evaluate investment IRRs and debt servicing capacity under multifactor scenario, layering sensitivity analysis and presenting results clearly.

Our recommendations leverage on Allied’s views regarding prevailing vessel values from our live floor of competitive shipbrokers blending in chartering data and other relevant market intelligence. The end-result is a responsible, pragmatic investment analysis which may be tweaked depending on other factors at th discretion of the recipient of our analysis.

Allied delivers maritime finance expertise with global reach and hands-on execution—advising on structure and negotiations, arranging a competitive capital raising process and coordinating every step to closing and drawdown.

Whether you’re evaluating a single-ship purchase, a refinancing, the introduction of a new lending relationship, or a multi-asset growth plan, partnering with Allied raises certainty, sharpens pricing, and helps making conscious choices.

Connect the dots with QuantumSea Research, Consulting and Valuations in making cutting-edge financing choices with the backing of our competitive ship and chartering brokers.